Microsoft (MSFT 0.43%) is one of a handful of hyperscalers that offer an astronomical amount of cloud computing capacity through hundreds of centralized data centers scattered all over the world. Microsoft rents this capacity to business customers via its Azure cloud platform, and many of them use it to develop and deploy artificial intelligence (AI) software.

Azure is consistently the fastest-growing piece of Microsoft’s entire business. However, investors are also focusing on the company’s AI virtual assistant Copilot, which is now embedded into flagship software products like Windows, Bing, and 365 (which includes Word, Excel, and Outlook). It represents a massive financial opportunity for Microsoft, but adoption has been modest so far, which has contributed to the recent sell-off in its stock price.

Microsoft stock is currently down 25% from its all-time high, but it’s now the cheapest it has been in more than three years. Should investors buy the dip, or is there more downside ahead?

Image source: Getty Images.

Are businesses shunning Copilot?

Copilot can be used as a regular chatbot, but it’s also a powerful productivity tool when packaged with enterprise software. Therefore, while anybody can use it for free through the Windows operating system or Bing search engine, Microsoft charges a fee if businesses want to embed it in the 365 application suite.

Companies currently pay for over 400 million 365 licenses for their employees (globally), so Microsoft has a massive addressable market for Copilot. But as of the tech giant’s recent fiscal 2026 second quarter (ended Dec. 31), businesses had only bought 15 million Copilot licenses for 365, implying a very modest penetration rate of just 3.7%.

On a positive note, that number grew by 160% year over year. Plus, the number of businesses with over 35,000 Copilot for 365 licenses tripled during the quarter, and daily active users soared tenfold. This suggests that once businesses adopt Copilot, they tend to introduce it to more of their employees over time and dramatically ramp up their usage.

Therefore, although some investors might be disappointed with the modest penetration rate for Copilot for 365 (hence the decline in Microsoft stock over the last few months), adoption rates seem to be trending in the right direction.

Azure’s blistering growth comes at a huge cost

Most AI development happens inside data centers, which house thousands of specialized chips supplied by companies like Nvidia. This infrastructure costs billions of dollars to build, which is why most developers rent computing capacity from cloud providers like Microsoft Azure instead.

Today’s Change

(-0.43%) $-1.75

Current Price

$408.93

Key Data Points

Market Cap

$3.0T

Day’s Range

$408.53 – $413.05

52wk Range

$344.79 – $555.45

Volume

1.8M

Avg Vol

33M

Gross Margin

68.59%

Dividend Yield

0.85%

As of Dec. 31, Microsoft had a $625 billion order backlog from customers who were waiting for more data centers to come online, which was up 110% year over year. That’s why the company has invested $118 billion to build more infrastructure over the last four quarters and will spend even more going forward.

However, there are concerns about the makeup of Microsoft’s huge backlog because 45% ($281 billion) is attributable to leading start-up OpenAI alone. That company only has around $20 billion in annualized revenue at the moment, and although it just secured $110 billion from investors in a recent capital raise, that still won’t be enough to fulfill its obligations to Microsoft — let alone the other cloud providers with which it has enormous outstanding commitments.

The good news is that Azure grew its revenue at a blistering pace of at least 39% in each of the last three quarters, and management says demand continues to exceed available supply. In other words, there appears to be more than enough customers to soak up any additional data center capacity Microsoft brings online in the near term. The longer term is more uncertain, but the company can always pull back on some of its planned spending if the demand environment shifts.

Microsoft stock is starting to look like a bargain

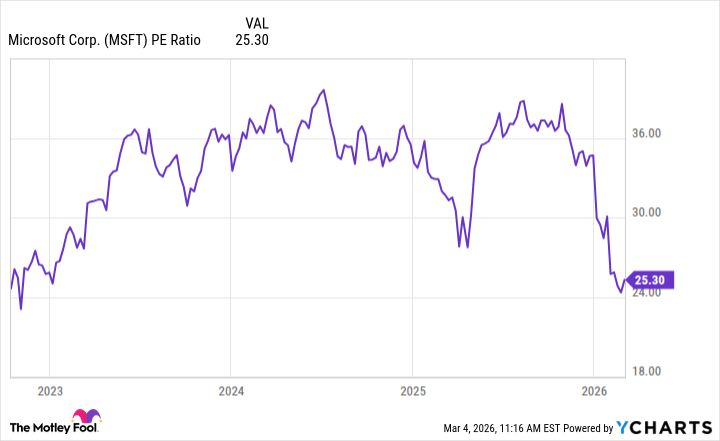

Microsoft produced earnings of $15.98 per share over the last four quarters, placing its stock at a price-to-earnings (P/E) ratio of 25.3. That is the cheapest level in over three years.

MSFT PE Ratio data by YCharts

Microsoft is now trading at a steep discount to the Nasdaq-100, which has a P/E ratio of 31.8, so it appears very undervalued relative to a basket of its big-tech peers. The stock is also inching toward a market multiple, since the S&P 500 (^GSPC 1.33%) currently trades at a P/E ratio of 24.7. Personally, I don’t think that makes sense, given Microsoft is one of the highest-quality companies America has ever produced, which is why it often trades at a premium to the rest of the market.

Opportunities to buy Microsoft at such an attractive price don’t happen very often, so it could be a great addition to any long-term stock portfolio.

Additional relevant updates

{kind=link}